- DAX Review

- U.S. Review

- Ryanair files anti-trust compliant

- Amazon 16 billion bond release

- Gigaset Earnings

- Economic Calendar

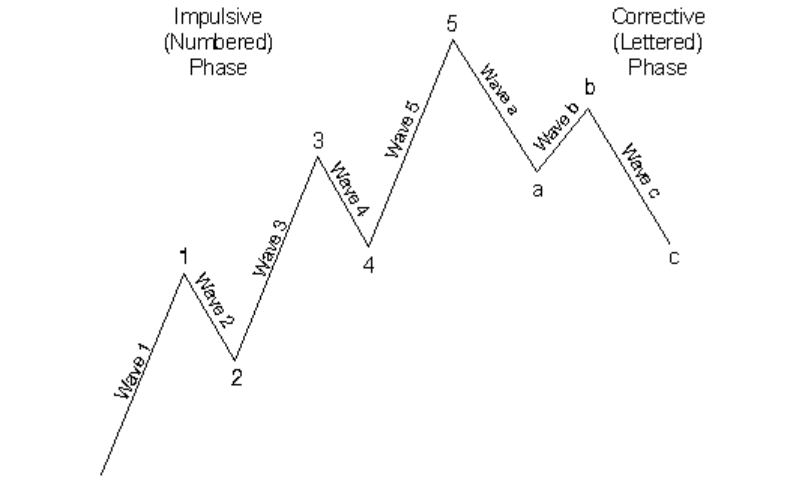

In case you missed out Elliott Wave Technical Analysis Report, make sure to catch up on it.

The DAX is recovering from its recent losses. 3 hours before close the German Index is up by 0,83% reaching the 12278 point mark. With this actual form it does seem that the DAX will be breaking its August high. There are no major international signals, as the Brent and Gold seem have to stabilized at 50 USD and 1270 USD respectively.

Following a strong equity market rally on Monday, as simmering tensions eased a little with North Korea, and fears of an imminent armed conflict with that nation lessened to a degree, Wall Street calmed down a bit yesterday morning, too. Indeed, after a small early extension to the rally in the first few minutes of yesterday’s session, stocks faltered somewhat within the first hour of trading, and an early 35-point gain in the Dow Jones Industrial Average quickly faded, with that blue-chip composite falling into the red during the second hour of trading. The other averages went into the red, as well. Meantime, a big individual story, one day after the shift away from North Korea, was at giant home improvement retailer The Home Depot, which issued quarterly results yesterday. And while the top and bottom-line results were better than expected, the gains, and the raised full-year forecast did not satisfy the Street, as that stock tumbled, losing nearly 4% of its value early on. The loss in HD turned the Dow negative, costing that index some 40 points. However, after that initial turn down by the Dow, that index returned to the black shortly thereafter. Also in the retail category weak earnings hurt Coach stock in early dealings. Still, the resilience of the bulls was evident yesterday, with that late-morning attempted comeback in the Dow. Meanwhile, in other market moving news, the Commerce Department reported that retail sales had posted an increase of 0.6% in July. That was above the 0.4% rise forecast. Also, June’s result was pared back from a rise of 0.4% to one of 0.3%. Excluding motor vehicle sales, core retail spending was ahead of 0.5%. Here, too, the gain was above consensus. Contributing to the pickup were sales of furniture and home furnishings, and building materials. Sales over the Internet soared, meantime, advancing by 1.3%. The market remained in somewhat of a mixed pattern as the noon hour arrived in New York, with the Dow near the breakeven line, and with the S&P 500 and the NASDAQ each off incrementally. The small-cap Russell 2000 and the S&P Mid-Cap 400 also were in the red, but in a more meaningful way. As has been the case recently, it was the retail group suffering once again, with steep losses in some high-profile names, such as Under Armour. Also, more stocks were lower than higher on the Big Board at that time, by a count of two-to-one while among the core groups, energy, basic materials, and consumer stocks were leading things lower. The weak tone persisted through the middle of the afternoon, and while the Dow held near the breakeven line, and the large-cap S&P 500 and the NASDAQ were just down incrementally, the smaller indexes and the advance-decline ratio were notably off. It was, to that point, a somewhat sobering day, even as the economy continued to show relative strength and the news out of North Korea was somewhat reassuring, for now. The equity market then would firm up slightly as the session wound down, but the overall weaker tone would persist into the close. When all the numbers were in, the Dow, with some last-minute selling, would end the session ahead by just five points; the S&P 500 would conclude matters just about where it began them; and the NASDAQ would end the day off seven points. Losing stocks easily led gains, though, and the small- and mid-cap categories showed noted weakness.

Germany on Wednesday rejected a claim by budget airline Ryanair of a conspiracy behind efforts to keep bankrupt rival Air Berlin afloat until a new owner is found. The Irish airline lodged a complaint with European Union competition authorities after Air Berlin filed for bankruptcy protection and then got a 150 million euro ($177 million) loan from the German government. Ryanair said late Tuesday there’s “an obvious conspiracy” between the German government, Lufthansa and Air Berlin. The loan will help Air Berlin to keep flights running for the next three months, while it is negotiating a possible deal with Lufthansa and another unnamed carrier, reported by German media to be easyJet. A spokeswoman for Germany’s Economy Ministry said it was “absurd” to claim that the rescue package had been staged. Beate Baron told reporters in Berlin that the government expects the loan to Germany’s second-largest airline to be repaid. Air Berlin filed for bankruptcy protection Tuesday after its main shareholder, Abu Dhabi-based Etihad, said it would make no more financing available following years of unsuccessful turnaround attempts. The airline, which carries some 80,000 people a day mostly on short-haul destinations, made a loss of about 782 million euros last year.

Amazon.com Inc. on Tuesday completed a $16 billion bond deal to fund its planned $13.7 billion acquisition of Whole Foods Market Inc. The issue came a day after ratings agency Moody’s Investors Service assigned the deal a Baa1 rating and revised Amazon’s credit outlook to positive from stable. S&P Global Ratings assigned the credit a higher rating of AA-minus last week. Amazon raised $16 billion in a seven-part offering that included a 40-year tranche, underwritten by Bank of America Merrill Lynch, Goldman Sachs and J.P. Morgan Chase. As expected, the bonds priced at the tight end of guidance, but the new concessions were still attractive, according to research firm CreditSights, which had upgraded its recommendation on Amazon’s bonds to outperform from underperform based on the initial price talk. Initial price talk on the 10-year tranche was 110 basis points above comparable Treasurys, which later tightened to Treasurys plus 90 basis points. CreditSights analysts led by Jordan Chalfin said at the price, the notes were still a bargain.

Gigaset reported a drop in first-half sales and EBITDA but reiterated its outlook for higher sales over the full year, thanks to growth in new market segments like smartphones. In the first half, smartphone revenues rose to EUR 3.7 million from EUR 1.1 million a year earlier, following the launch of two devices. Over the first six months of 2017, total revenues fell 3.6 percent to EUR 128.3 million due to a continued contraction in Gigaset’s main market, cordless home phones. Sales in the consumer segment fell to EUR 98.1 million from EUR 110.7 million a year ago, while the business market grew 25.7 percent to EUR 25.4 million, driven by strength in its home market Germany. EBITDA fell to EUR 5.7 million from EUR 10.6 million in the first half of 2016, hurt by increased spending on marketing and R&D, including the ramp-up of mobile sales. Excluding the extra EUR 4.6 million in costs, EBITDA would have been largely stable for the full year, Gigaset said. Free cash flow was a negative EUR 24.1 million versus an outflow of EUR 13.1 million a year earlier. Despite the lower H1 results, Gigaset maintained its outlook for higher revenues over the full year, with a low double-digit million euro increase thanks to the expanding smartphone business. Core EBITDA is expected to reach EUR 15-25 million over the year, while cash flow should be just a mid single-digit million euro outflow.

Today Economic Calendar:

- MBA Mortgage Applications

- Housing Starts

- Atlanta FED Business Inflation Expectations

- EIA Petroleum Status Report

- FOMC Minutes