Initial Comments:

So I have decided to post this article as a Weekend Special Edition. Bitcoin is a topic that I have invested a lot of time in myself. This article is a long read for people who really want to try and understand the Bitcoin technology.

As there is no uniform terminology we will refer in this article to Bitcoin as the technology and to bitcoin as the underlying currency itself.

This article will be solely focused on Bitcoin and the underlying Blockchain and is divided in 5 sections:

- Introduction

- What is Bitcoin? How does the Blockchain work?

- Is the Bitcoin setup impenetrable?

- An empirical analysis on the usage of bitcoins.

- Valuation of bitcoins

- Introduction

Bitcoin is a digital currency that creates unique, non-duplicable electronic tokens using software (dubbed mining) with an asymptotic limit of creation of 21 million tokens. Every four years the number of bitcoins created is scheduled to be cut in half until 2040 when creation is supposed to go to zero. The system operates by clearing transactions in a peer-to-peer decentralized system. If you don’t understand the previous sentences, it’a fine as we will come to the core of Bitcoin and the workings of the underlying technology. Since Bitcoin first started trading (on stock exchanges) the 16th of July 2011 the price has increased by baffling 5’209’254% (as of 29.06.2017). Officially Bitcoin was introduced to public in 2009, when Satoshi Nakamoto (allegedly a pseudonym) introduced his whitepaper entitled :”Bitcoin: A Peer-to-Peer Electronic Cash System”.

The bitcoin has enjoyed an enormous increase in valuation, reaching a total market capitalization of 40 billion USD. As shown in the graph above Bitcoin surged for the first time in November of 2013 reaching an all time-high, at a market cap of 13,9 billion USD. Bitcoins plummeted afterwards and hit the floor on a market cap of 2,4 billion USD. On the 11th of June 2017 bitcoins rallied up to a record-breaking 2895,44 USD. Given this recent , nearly unseen rise, it’s astonishing that many people don’t understand what Bitcoins are and how they work. In this article we will try to get to the core of Bitcoin and the underlying blockchain, we will support our assumptions with empirical analysis. One resource will be the whitepaper released by Satoshi Nakamoto. As the concept of Bitcoin is technically complex we will be quoting the most relevant extracts, try to paraphrase them and supplement them with practical examples. If you are a curious and tenacious mind I suggest you read Nakamotos paper yourself.

2. What is Bitcoin? How does the Blockchain work?

“A purely peer-to-peer version of electronic cash would allow online

payments to be sent directly from one party to another without going through a

financial institution.”

This first quote is taken from the abstract and elaborates on the Bitcoins doctrine, a decentralization of cash-flow. Our current methods of making transactions require our money to go through Financial Institutions such as Banks, the FED or any other governmental institution. For years we have trusted financial institutions as middlemen for all of our transactions, the repercussions can be enormous as history has proven. In 2015 Greece was facing a sovereign default, with the Banks having no liquidity and with no re-financing possibilities at first. People were standing on the streets, raiding every ATM they could find in the hopes of saving what was left on their bank deposits. The Greek Government debt crisis has various catalysts, among them a corrupt government and rigged banks. Private Greek banks started according dubious loans and creating a credit bubble that burst in 2010. Two years beforehand Lehman Brothers, a real estate hedge fund disguised as an investment bank, was the originator of the subprime-mortgage financial crisis when it filed for bankruptcy on the 15th of September 2008. By that time, Lehman had assets of $680 billion supported by only $22.5 billion of firm capital. From an equity position, its high risk commercial real estate holdings were three times greater than capital. In such a highly leveraged structure, a three- to five-percent decline in real estate values would wipe out all capital, which finally ended up by happening and causing a financial mayhem . So this really begs the questions: “Why do we entrust banks with our money?”. Because we plain and simply lack alternatives to them. Clearly having all our financial transactions , like loans, credit transactions and savings-account, handled by banks bears a concentration risk. Projects like Kickstarter have been a real alternative to banks, crowdfunding projects thus replacing the process of inquiring for loans at banks. What Nakamoto proposes is that there is a possibility to replace banks as middlemen for online transactions. If we think about electronic money transfer, we have to think this process is just an entry in a register, as no physical cash gets exchanged. If we are able to set-up a public and anonymous register, are we then able to construct an online transaction network without middlemen?

“Commerce on the Internet has come to rely almost exclusively on financial institutions serving as trusted third parties to process electronic payments. While the system works well enough for most transactions, it still suffers from the inherent weaknesses of the trust based model.”

This paragraph extracted from the Introduction accurately pinpoints which problems need to be faced to institute a decentralized network. Nakamoto proposes that the “inherent weaknesses of the trust based model” is a hurdle to online transactions. Completely non-reversible transactions are not possible, since financial institutions cannot avoid mediating disputes. The cost of mediation increases transaction costs, limiting the minimum practical transaction size and cutting off the possibility for small casual transactions. With the possibility of reversal, the need for trust spreads. Merchants must be wary of their customers, hassling them for more information than they would otherwise need. A certain percentage of fraud is accepted as unavoidable. Nakamoto suggests that the trust-model should be replaced by a mathematical model. We will now slowly start to dig into how the blockchain works.

Imagine you are a group of 5 friends sitting in a circle. Everyone in the circle has a sheet of paper and a pen. Friend A wishes to make a 10 euro transaction to friend B. He will now say it out loud and notify the whole group. Everyone in the group verifies if friend A has enough balance to pay friend B and then takes note of the transaction. Whenever enough transactions have been made and documented, all friends put their respective page away in their own folders and start a new one. As you might be able to tell everyone will store away the same amount of information. But before putting away the page, the group of friends needs to make sure that no one can alter the content of what has been documented. The pages need to be sealed with a code that everyone in the group agrees to. In the Bitcoin jargon the process of sealing is defined as mining.

“We define an electronic coin as a chain of digital signatures.”

This is where it starts getting technical. Firstly we will have a closer look at hash functions, as they are the main component of the mining process. A hash function is any function that can be used to map data of arbitrary size to data of fixed size. Suppose you have the number 100 as an argument and run your hash function on it. The output will be “ghakjdhg”. Given our argument that we have now defined as 100. the output will always be the same, in this case “ghakjdhg”. No one will know how your argument got converted into “ghakjdhg” and moreover the process is irreversible, eliminating any possibility of backtracking the functions logic. This means that given the word “ghakjdhg”, it is impossible to tell what our input was, hence why hash functions are very helpful in cryptography. As you might have figured out, hash functions play a role when it comes to Bitcoin mining. To illustrate the usefulness of hash functions in the mining process we will come back to our example with the group of friends. Let’s assume that the total sum of all transactions on one page is equal to 275 Euro, so we label this page with the number 275. Then we will try to find a second number that when added to our number gives us an output of that starts with 4 a`s. After some calculation we may find that this number is 45678. In such a case, 45678 will become the seal for the number 275. To seal the page that bears the sum of 275 euros we will put a badge labeled 45678 on it. An altering of the transaction sum, to lets say 300, would change the output of the hash function. The sealing of numbers is called proof-of-work, as defined in chapter 4 of Nakamotos paper .

“To implement a distributed timestamp server on a peer-to-peer basis, we will need to use a proof-of-work system similar to Adam Back’s Hashcash, rather than newspaper or Usenet posts.The proof-of-work involves scanning for a value that when hashed, […] , the hash begins with a number of zero bits.”

So we have come to the conclusion that the combination of the sealing number and the total sum of transaction gives us a unique output. But who calculates the sealing number? Let’s go back to our group of friends, who has just finished another page of transactions. Everyone in the group engages in the process of calculating a matching sealing number. The first to figure it out will then announce it to the rest of the group. As soon as the sealing number gets announced everyone double-checks if it yields the required output or not.

Some readers now might be asking themselves: “Why should I waste time and energy figuring out a sealing number if eventually someone else might do it?”. This problem gets addressed in Chapter 6, named “Incentive”. Obviously in the real world the process of finding the adequate sealing number, takes up electricity and deteriorates your GPU and/or CPU. The twist is that the first one to calculate the sealing number gets compensated for his success. So imagine we get back to our circle of 5 friends and friend C is able to calculate the sealing number. Friend number C will be rewarded with a freshly printed 1 Euro piece for his efforts, effectively not decreasing anyone’s balance (disregarding any inflationary effects).

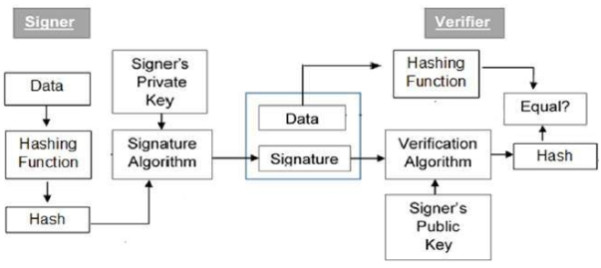

We will now advance to digital signatures and how they are embedded in the Bitcoin network. Digital Signatures play a critical role when sending and receiving bitcoins. Digital signatures are the public-key primitives of message authentication. In the physical world handwritten signatures are used to make contracts or documents binding. Similarly, a digital signature is a technique that binds a person or an entity to some sort of digital data and is much less susceptible to fraud.This binding can be independently verified by the receiver as well as any third party. A digital signature is a cryptographic value that is calculated from a secret key, belonging to the signer.

Depicted above we are able to see the flow of a standard normal digital signature process.

Each person involved in the signature flow will have a public and a private key pair. Generally the key pairs used for encryption/decryption and signing/verifying are different. The private key used for signing is referred to as the signature key and the public key as the verification key. The signer feeds some data to a hash function and generates a hash of that data. After obtaining a hash value, its is packed together with the signature key and the package is then fed to the signature algorithm. The algorithm will then proceed to create the digital signature. The signature is appended to the data and both are then sent to the verifier. The verifier then feeds the digital signature and the verification key into the verification algorithm. The verification algorithm gives some values as output, meanwhile the verifier also runs the same hash function on the received data to generate a hash value. This hash value and the output of the verification algorithm are compared. Based on the comparison result, the verifier decides whether the digital signature is valid. The digital signature will be unique, as it is created by the verifier’s private key.

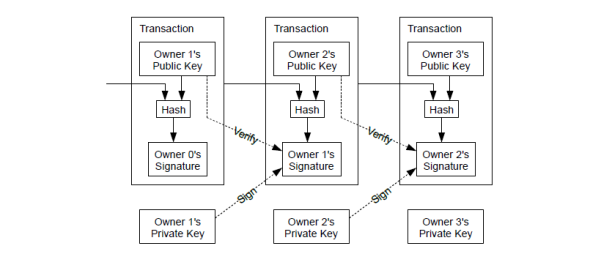

“Each owner transfers the coin to the next by digitally signing a hash of the previous transaction and the public key of the next owner and adding these to the end of the coin. A payee can verify the signatures to verify the chain of ownership.”

To illustrate the Bitcoin transaction procedure we will annex the process flow chart from Nakamotos paper.

For person 1 to transfer a coin to person 2, person 1 signs the hash of the last Bitcoin transaction to occur and the public key of Person 2. Because the network is high-velocity, most of the major parts in the Bitcoin network are high performance supercomputers and dedicated servers that have enough processing power to manage all of the transactions across the continents.

It stands out that bitcoin transactions are very unique in the sense that transactions can be made between parties on opposite sides of the globe via the Internet. Due to the underlying mathematical models no middlemen, such as banks, are needed anymore.

3. Is the Bitcoin setup impenetrable?

While bank robberies and money counterfeiting are of course no problem for an electronic currency, Bitcoin online platforms face severe hacker attacks. Furthermore, due to the lack of regulation the Bitcoin ecosystem remains a “Wild West”. Because Bitcoin transactions are non-revocable, hackers have frequently stolen bitcoins of individuals leaving the victims without recourse. The most common source of scourge to afflict Bitcoin participants has been the denial-of-service attacks (DDoS). These are inexpensive to carry out and quite disruptive. Records show that competing services carry them out in order to improve their market share. A massive DDoS attack hit OKCoin, a China-based Bitcoin exchange, the 10th of July 2015. The platform saw a massive distributed denial of service attack on the which resulted in the international site being shut down for a week. Furthermore the platform compensated traders for losses incurred due to the DDoS. Other times exchanges similar to OKCoin have just shut down without explanation, often with customers losing their deposits. Empirical papers like Vasek et al (2014) show, the number of attacks has increased over time. Böhme et al. (2015) argue that DDoS attacks are especially attractive as stolen Bitcoins can easily be converted into money. We will not dwell into the depths of how such attacks occur but have a look at their frequencies and repercussions. Despite their apparent frequency, very little is known about the true prevalence of DDoS attacks.

From May 2011 to October 2013 142 DDOS attacks on 40 Bitcoin services were documented. Most currency exchanges and mining pools are much more likely to have a DDoS protection such as CloudFlare, Incapsula or Amazon Cloud. Vasek et al (2014) found that 7% of all known operators have been attacked, but that currency exchanges, mining pools, gambling operators, eWallets and financial services are much more likely to be attacked than other services. The study found that big mining pools (those with historical hashrate shares of at least 5%) are much more likely to be DDoSed than small pools.

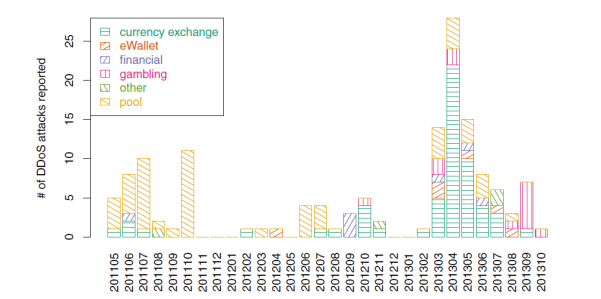

This Graph issued by Vasek et al. (2014) plots the shift in the DDoS attack targets. We can see that the number and target of reported attacks varies greatly over time. Initially, in the second half of 2011, most DDoS reports concerned mining pools. Then there were very few reported attacks of any kind during the first half of 2012. During the second half of 2012, DDoS attacks picked up again, initially targeting pools, but more frequently targeting currency exchanges and other websites. During 2013, attacks on pools continued, but they were joined by DDoS on gambling websites, eWallets, and currency exchanges. Attacks on currency exchanges dominated the totals from March–June 2013, coinciding with rising exchange rates and unprecedented interest in Bitcoin.

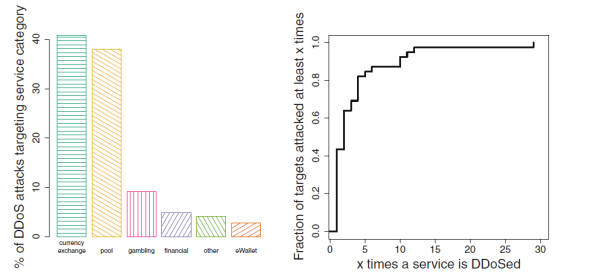

This second table, also published by Vasek et al. (2014), allows a categorisation of DDoS events. Currency exchanges and mining pools make up for nearly 80% of the DDoS attack targets, whereas gambling sites make up for 9%. The figure on the left depicts a cumulative distribution function off how recurrent DDoS attacks are on certain entities. It can be observed that 44% are only attacked once while 15% are attacked on at least on five different occasions. The leader in suffered DDoS attacks was Mt. Gox, with 29 suffered attacks. Mt. Gox was responsible for almost 90% of all the exchange operations in the network before filing for bankruptcy. Mt. Gox has filed for bankruptcy protection from creditors in February of 2014. In April 2014, the company began liquidation proceedings. Out of the 1236 Bitcoin related services only a mere 203 services (16%) have adopted an Anti-DDoS application. The adoption rate among services who have been hit by DDoS attacks is with 54% comparably higher, nonetheless still considerably low.

The Bitcoin’s Proof of work system has been developed to prevent double spending schemes. A double spend attack, is a scheme which enable a certain set of bitcoins to be spent in more than one transaction. Karame et al. (2012) have been able to show that it is possible to bypass the proof of work. While the Bitcoin payment verification process is designed to prevent double spending, Karame et al. show that the system requires tens of minutes to verify a transaction and is therefore inappropriate for fast payments. The security of using Bitcoin for fast payments was analyzed. The paper shows that unless appropriate detection techniques are integrated in the current Bitcoin implementation, doubles spending attacks on fast payments succeed with overwhelming probability and can be mounted at low cost.

4. An empirical analysis on the usage of BTC’s.

We will now take a closer look at what bitcoins are used for and by whom. There are many types of statistics and graphs about the Bitcoin network which can be readily downloaded from the Internet (https://blockchain.info/charts). However these types of statistics tend to describe some global property of the network over time such as the number of daily transactions, their total volume, the number of bitcoins mined so far and the BTCUSD exchange rate. It is very difficult to get accurate information about how bitcoins are used in practice. A paper released in 2013 by Dori Ron and Adi Shamir entitled “Quantitative Analysis of the Full Bitcoin Transaction Graph” provides a detailed understanding off the Bitcoin network . This paper gives a great insight off all transactions from the first time Bitcoins became fully operational up to the 13th of May 2012.The data was gathered from the Bitcoin wallet, which tracks all transactions anonymously Even though the landscape, as of 2012, might have changed this paper provides a great insight towards the typical behaviour of users.

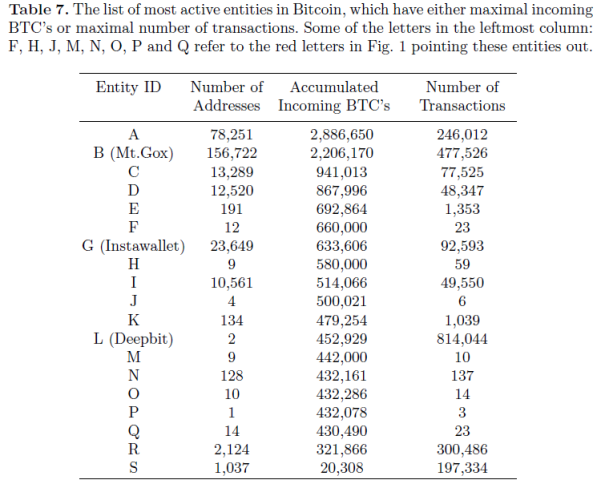

At the time there were 3’730’218 different public keys. 3’120’948 of them were involved as senders in at least one transaction, while the rest of 609’720 appeared to form a network of receivers. One entity (person or company) can have multiple Bitcoin addresses. The paper determined that the total of 3’120’948 addresses can be attributed to 1’851’544 entities. Adding the 1’851’544 entities to the network of receivers only we get a total of 2’460’814 entities involved in the Bitcoins transactions. This implies that on average every entity has 1,5 addresses. However there is a huge statistical variance in the number of addresses an entity manages and in fact one entity is associated with 156’722 different addresses. The paper was able to determine the entity behind all these addresses as being Mt. Gox. The paper made one very interesting finding regarding the distribution of Bitcoins. Of the 9’000’050 bitcoins that were in circulation 7’019’000 bitcoins could be attributed to the 609’720 addresses which only receive and don’t send any bitcoins which were almost 78% of all existing bitcoins. 76.5% of these 78% (or 5’369’535 bitcoins) are what is defined in the paper as “old coins”, this meaning that these coins have not been moved over a time-period of 3 months. The analysis of the total volume of transactions resulted that 40% of all addresses had received fewer than one bitcoin and 59% of the addresses had received fewer than 10 bitcoins over their lifetime. Bitcoin allows for micro transactions, which are called satoshi and are of the order of 10^(-8), this is the smallest fraction into which a bitcoins can be broken up. The paper also goes to show that on the other end of the distribution there was only one address which received over 800’000 bitcoins. The current balance of almost all 98% of all entities was less than 10 bitcoins. 93% percent of all addresses had fewer than 10 transactions each, while 80 addresses used the network for more than 5000 transactions. The paper also goes ahead and dissected the nominal of each transactions. 84% of all the transactions involved fewer than 10 bitcoins. On the other hand large transactions are rare with only 340 transactions larger than 50’000 BTC’s. The paper also went ahead and filtered out 19 of the most active entities. I attached the Table below.

Source

The table shows that Mt. Gox had the most addresses but not the largest accumulated incoming bitcoins nor the largest number of transactions. Six out of the 19 entities have each made fewer than 30 transactions with a total volume of more than 400’000 bitcoins each. A fair conclusion that we can draw from this paper is that most of the mined BTC’s remain dormant in addresses which had never participated in any outgoing transaction. We can also concluded that there is a huge number of tiny transactions which move only a small fraction of a single bitcoin, but there were also hundreds of transactions which moved more than 50’000 bitcoins.

Bitcoin has also been massively linked to the Silk Road in the past, an anonymous, international online marketplace that operates as a Tor hidden service in the past. “More brazen than anything else by light-years” is how U.S. Senator Charles Schumer characterized Silk Road which was shut down March 2015. The Silk road had reportedly between 30’000 and 150’000 active users. The Silk Road was an online “black market” which offered a variety of goods but had a clear focus on drugs. The users were able to stay anonymous, bitcoins granting anonymity even trough the payment process.

5. Valuation of bitcoins

As of now we have only been assessing the design and the technology underlying the decentralized infrastructure of Bitcoin. As this is a financial-centered blog we will try do identify if there are any valuation models for bitcoins. To be able to assess if we can erode a bitcoins value we elaborate whether Bitcoin is primarily an alternative currency or just a speculative asset. According to Kaplanov a currency can be used as a mean of trade, a vehicle to store value, or a unit of account in order to compare the value of different goods or services. Dirk B. et al state that:

“Bitcoin cannot be considered a currency. Its high level of volatility makes a reliable exchange impossible and adversely affects the store of value and unit of account properties. In addition, the fact that it is not an official currency in any country and not backed by any government implies that the high level of volatility affects every Bitcoin transaction, within-country and cross-country transactions. […] Hence, Bitcoin might better be classified as an investment. Its appeal lies in the large historical price movements and expected future returns. Whilst most assets exhibit at least some fluctuations of its price and can thus be labeled risky, Bitcoin appears to be particularly risky and clearly belongs to a high-risk (speculative) asset class.”

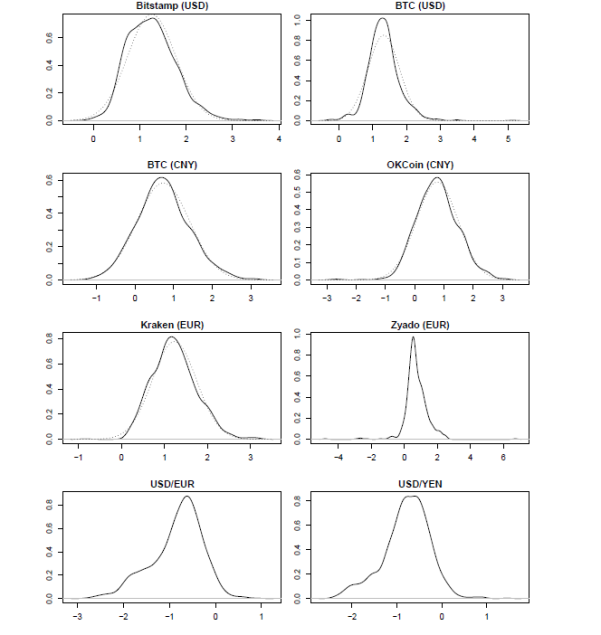

Speaking in terms of exchange rates an empirical analysis on volatility shows that minima and maxima observed average daily return for Bitcoin are about 10 times higher than for the Euro or Yen.The standard deviation of realized volatility for the Bitcoin markets varies between 229 and 558 basis points per day, which is 100 times higher than in the FX markets. The Euro FX market exhibits an average of volatility of 50 basis points per day. The figure, published by Dirk B. et al shows that all markets but BTC and Zaydo, from the chosen sample these had the lowest market shares, exhibit moderate statistical skewness. For those two markets the chosen samples show a leptokurtic distribution.

As bitcoins do not provide the feature of an interest rate in contrast to traditional currencies, where interest rates are provided by central banks, valuation models relying on given interest rates are rendered meaningless. Users are left to determine the value of bitcoins themselves by gathering and evaluating information in news and web resources. The price is therefore determined on exchanges by demand and supply. Considering that there is a cap at 21 million bitcoins, as of 8 February 2017 there were 16’152’087,5 bitcoins in circulation, off which many may be lost or not in circulation, it follows that an increasing growth of the demand side is leading to increasing prices. An example how prices can be driven up by an increasing demand can be exemplified with Baidu. On October 14, 2013, Baidu, a web services company that runs the largest search engine in China, began accepting bitcoin. This single action opened the bitcoin network to roughly 570 million internet users in China and prompted other internet companies to consider the cryptocurrency more seriously. The closing price of bitcoin, which averaged just $124 over the 2-week period prior to the announcement, increased to $170 over the 2-week period following the announcement. As we have seen recently the mixture of media attention, the novelty of both the design and the features of a cryptocurrency, combined with its global availability over the internet , have lead to an exponential growth of demand. It seems to be a fair assumption to say that an increase in the number of Bitcoin participants is associated with an increase in the Bitcoin network volume, leading to an increase in the Bitcoin price. It follows that if Bitcoin participants seek to use Bitcoin primarily as an asset, they will not leave a footprint within the Blockchain. This is supported by the common practice of exchanges to keep internal accounts on behalf of their customers. That is, the exchanges are handling accounts of their customers in an internal accounting system, guaranteeing for keeping record of the on-exchange purchased and sold Bitcoins without actually transferring these Bitcoin through the Blockchain. We would expect that those users’ Bitcoins primarily remain within the exchange internal systems.

Users pursuing Bitcoin for its purpose as an alternative asset also lack a valid valuation method. Given that there is no fundamental pricing methodology available, sources of information, like the media, are likely to have a higher influence on prices. Negative news like the announcement of security issues revealed in the underlying protocol should concern users who are using Bitcoin for operational transactions and push some users to re-evaluate the utility and usability and eventually sell their Bitcoin, hence lowering prices on exchanges. Due to the volatile character and the volatile historical prices of the underlying an investor may be aware that they invest in an instrument with a high price uncertainty. Hence, it is a valid assumption that these users only invest a small amount of their total portfolio. They buy Bitcoin at an exchange and store it, waiting for prices to rise. An investor might also keep in mind that if Bitcoin is rendered illegal by change of law, the Bitcoin immediately lose their value. What seems to be noteable is the correlation between the price of Bitcoin and the daily English Bitcoin Wikipedia views, which has been pointed out by Florian Glaser et al. in 2014. This graph helps to identify the mass of particularly uninformed users who have only limited knowledge about Bitcoin and therefore acquire initial information from an initial source of information like Wikipedia.

View at Medium.com